When Sir Bob Geldof toured Australia in 2015, the Irish rocker and social activist spoke about how global “flashpoints” of conflict were ultimately caused by great change and poverty, and he spoke about the rise of internet mega giants Facebook and Google and the distractions of the 24-hour news cycle for political leaders.

In doing so he made a connection between the industrial revolution and the technology and information revolution we are experiencing and the resulting disruption of the status quo that is already underway.

It is estimated that 40% of the current jobs will disappear, traditional employment models will slowly be eroded and people will be paid on the basis of the value they deliver, rather than the hours worked.

Harnessing disruption and creating value

Rachel Botsman, a global authority on the power of collaboration and sharing to change the way we live, work, bank and consume, states that this is not a technology trend, but is rather a transformational lens.

Rachel describes three reactions to the disruption of the collaborative economy:

- Ostrich – hope it will all go away (head in the sand)

- Fight – (Try to bring new idea down with legal action)

- Pioneer – or you can embrace change as an opportunity and pioneer.

Now you might be thinking this is about consumer goods and services, it doesn’t apply to my industry. This is the Ostrich reaction.

Eastman Kodak experienced the consequence of behaving like an Ostrich. Perversely they were the company that developed much of the digital technology that today’s digital cameras are based on, but feared the technology would damage their film manufacturing business and delayed developing products. When it became obvious a digital world was developing (great pun), they began to divest the traditional chemical industry aspects of their business to concentrate on their digital technology only to find they could not compete as technology hardware manufacturers.

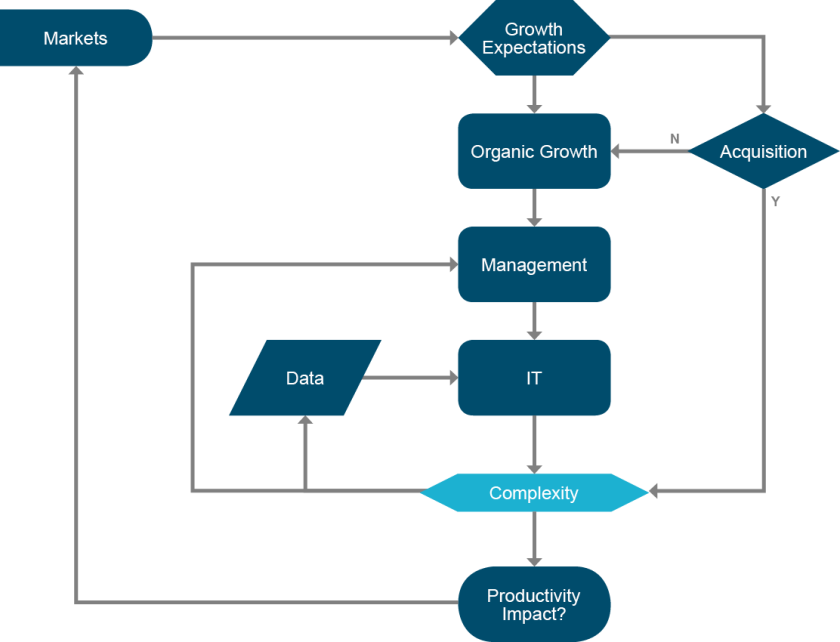

At TAM we have coined the term ‘Contagion of Complexity’ to describe the complexity resulting from unthinking pursuit of growth above the organic, the consequent cyclical growth in management and IT, and the subsequent cyclical battle with the law of diminishing returns.

There is a point of inflexion where the pursuit of scale is limited by the law of diminishing returns. Entire societies have collapsed this way, let alone major companies.

At TAM we see this downward cyclical trend as the opposite of our upward spiral of excellence. In other words, our collaboration is focussed around ensuring growth results in improved productivity through the intelligent application of technology, business process, technical excellence and people development.

Can the transformational lens of collaboration be applied across all industry sectors to understand the opportunities to become leaner and more efficient? Boom and bust may be a reality, but nothing stops us taking the opportunity to position for boom whilst gaining efficiency in a bust.

In fact it seems to us that the macro economic cycles are driven by the changes that if embraced allow us to profit during bust and grow during boom. Technology driving changes in oil prices would be a classic.

You only have to look to collaborative companies such as Uber and Airbnb to understand that reimagining your business model can unlock a hidden wealth of productivity, capacity, innovation and value.

This is what we have done at TAM. We have chosen to apply the sharing economy model to professional services. The same drivers for the establishment of cooperatives during the industrial revolution are just as valid in the technology revolution of today. The technology enables specialisation, creating the opportunity for knowledge workers to deliver value as individuals rather than employees.

Rewarding individuals in proportion to the value delivered means people work fewer hours. This creates a constructive culture more suited to today’s age of automation and achieves a better work life balance for the individual.

By cooperating, exchanging combined knowledge for value and embracing disruptive technologies industry as a whole has an opportunity to achieve a step change in efficiency, capacity, performance and innovation.